Deko is a multi-lender payment platform designed to enable flexible checkout finance for both merchants and consumers. Its core proposition is to support any basket, anytime, anywhere, allowing businesses to offer tailored financing options seamlessly within the purchasing journey.

The platform connects multiple lenders in a single ecosystem, intelligently matching customers with suitable finance options to improve conversion rates and create a smoother checkout experience. By centralising lender integrations, Deko reduces complexity for merchants while increasing accessibility to finance for end users.

With a strong focus on scalability and continuous expansion, Deko evolves its offering to meet diverse business needs, positioning itself as a trusted partner in retail finance. Its product culture is grounded in clear values - doing the right thing, being bold, and operating as one team - which support collaborative delivery and customer-centric decision-making.

Digital Credit Account

Embedding finance into the shopping experience through a credit-first model.

Overview

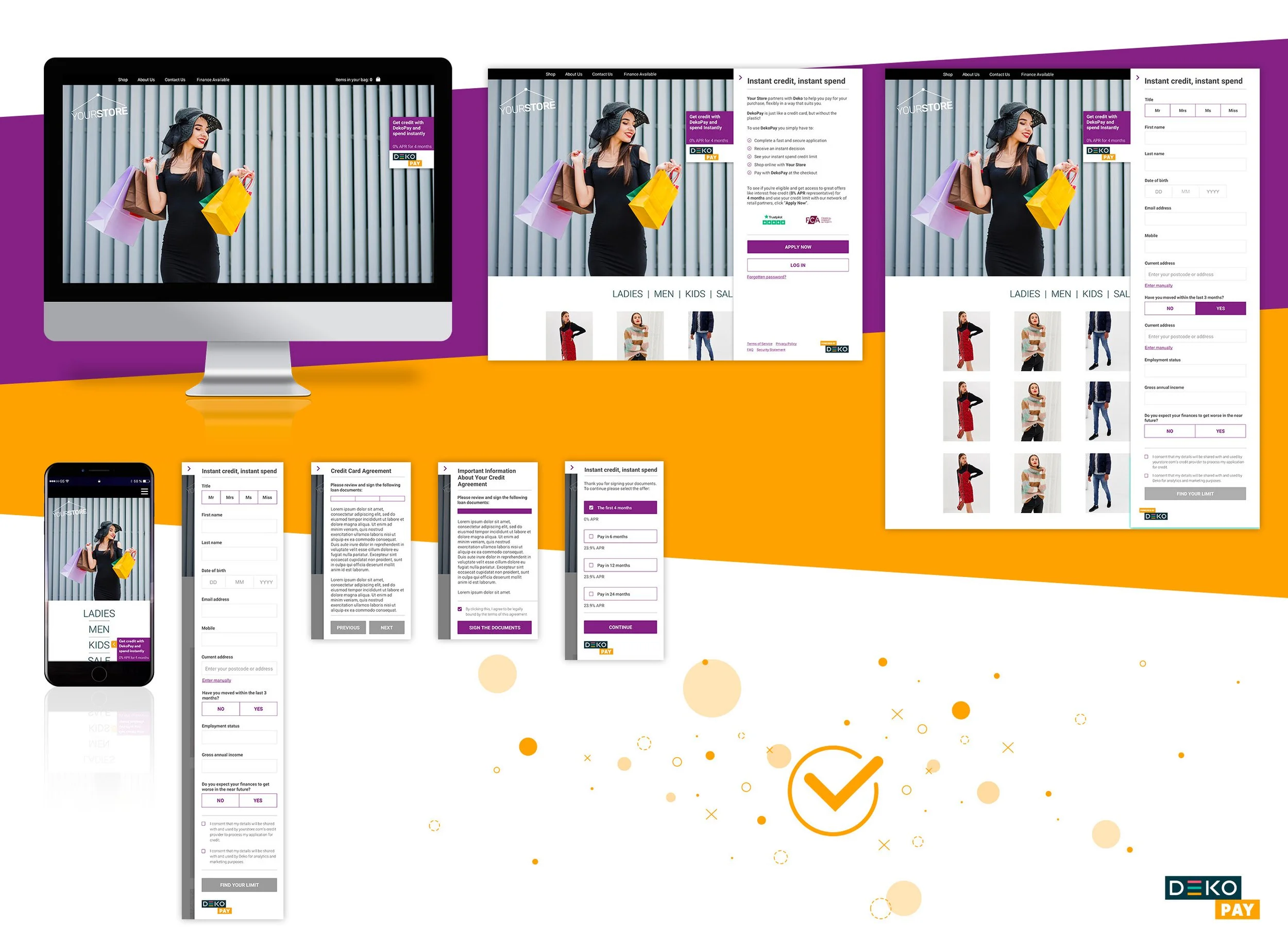

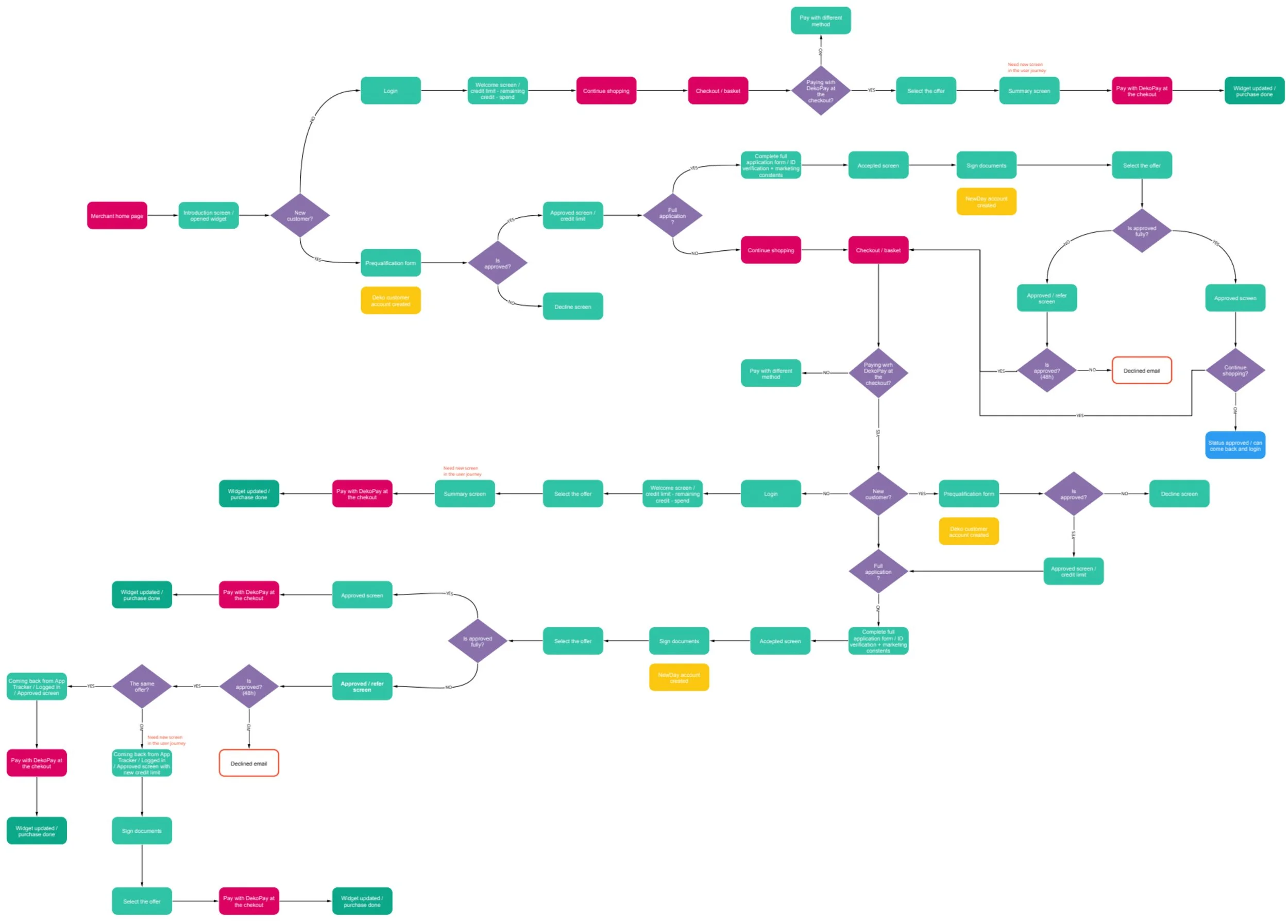

The Digital Credit Account was designed as an evolution of the pre-qualification and affordability tools, shifting finance from a checkout step to an integral part of the shopping experience. The product enabled customers to understand their available credit upfront and use it seamlessly during their purchase journey. Positioned directly on merchant websites—such as homepage or product pages—it allowed users to make more confident purchasing decisions before reaching checkout. Developed in collaboration with a lending partner, the solution combined pre-qualification, credit access, and account management into a single, cohesive experience.

My Role

Product Designer

I contributed across the full product lifecycle, including:

facilitating and participating in a 5-day design sprint

shaping product direction through workshops and discovery

designing high-fidelity prototypes and final UI

iterating based on user testing and stakeholder feedback

collaborating with product, engineering, and external partners

Team Structure

The product was developed within a cross-functional team, including:

Product Designer (my role)

Product Managers

Frontend and Backend Engineers

QA (in later stages)

The initial concept was developed during an intensive design sprint, bringing together design, product, and engineering from the outset.

The Challenge

The core challenge was to design a product that would deliver value across three interconnected stakeholders:

Customers, who needed clarity and confidence around affordability

Merchants, who aimed to increase conversion and basket size

Lenders, who required scalable and responsible lending mechanisms

We wanted to reduce friction in the application process while increasing customer confidence and engagement, ultimately improving conversion and retention.

However, the problem space introduced several complexities:

unclear user expectations around credit usage and flexibility

varying merchant needs depending on industry

shared responsibility for customer communication between platform and lender

balancing simplicity of experience with financial and regulatory requirements

To explore these uncertainties, we initiated a design sprint to rapidly define and test the product concept.

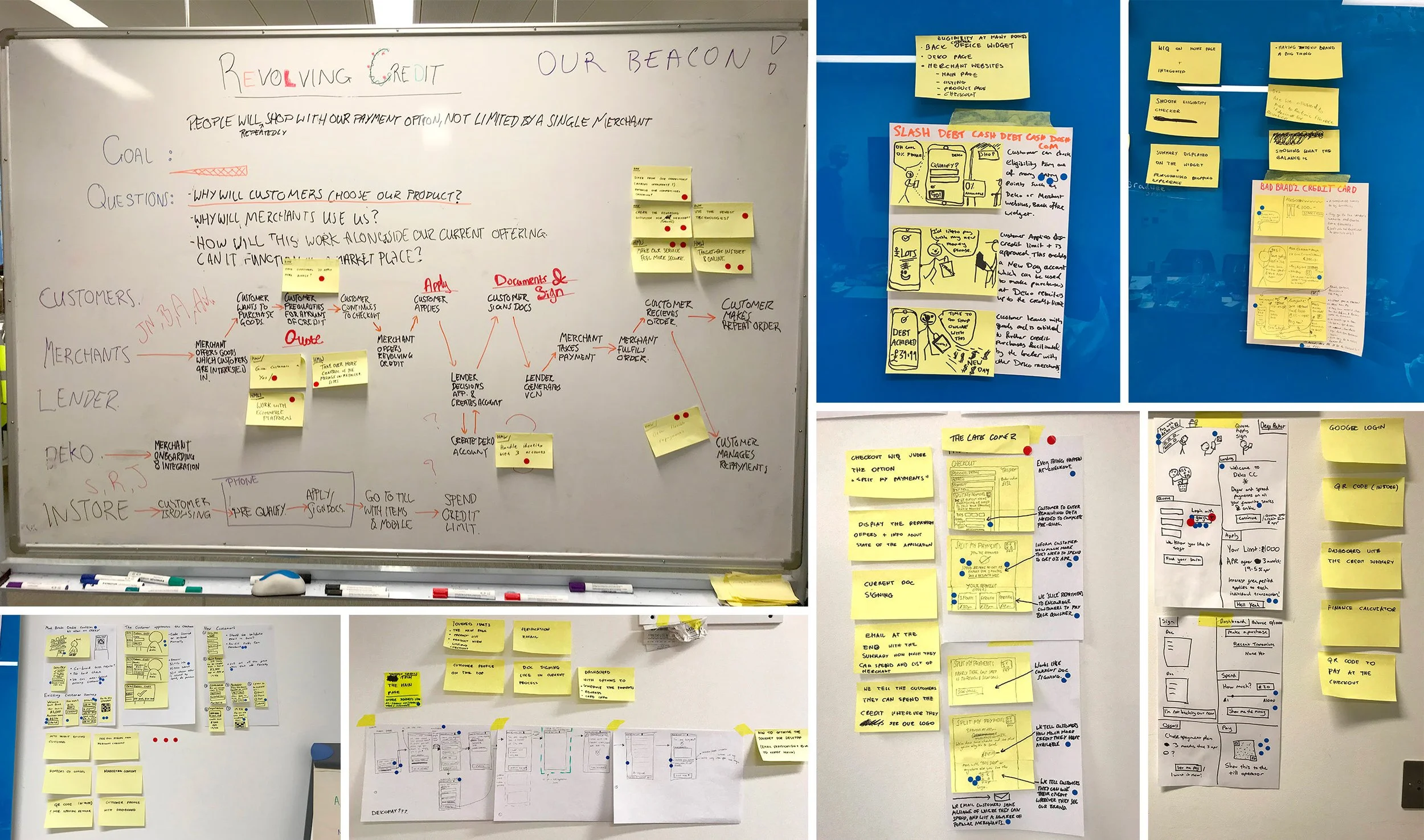

Design Sprint & Discovery

The product concept was developed and validated through a 5-day design sprint, bringing together product, design, and engineering.

Throughout the sprint, we:

mapped the problem space and gathered expert insights

explored multiple solution directions through sketching and ideation

aligned on a single concept and created a detailed storyboard

built a high-fidelity prototype

tested the concept with users to validate assumptions

The sprint allowed us to move quickly from idea to validated concept, reducing risk before committing to development.

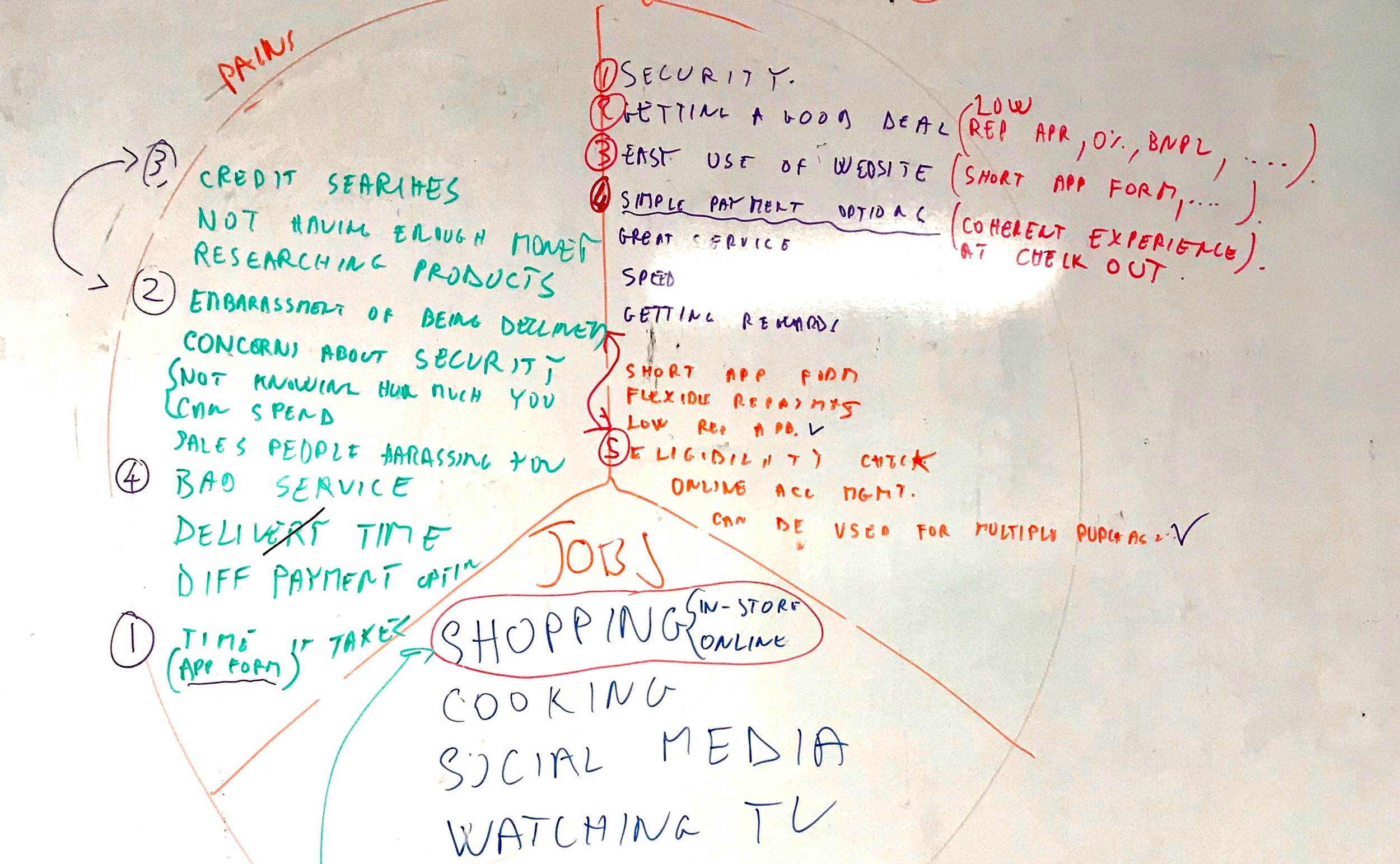

Key Insights

User testing revealed several critical insights that shaped the product direction:

Users valued flexibility in how and where they could spend credit, rather than being restricted to a specific merchant ecosystem

Presenting a fixed credit limit upfront was less effective than enabling context-specific financing decisions

Simplicity and clarity in the application process were key to maintaining engagement

These learnings led to a refinement of the original concept, ensuring the product aligned more closely with real user expectations.

Product Definition & Iteration

Following the sprint, we continued discovery through workshops focused on viability, feasibility, and value proposition.

We worked to:

define clear ownership across stakeholders (platform, lender, merchant)

refine the end-to-end journey to ensure a seamless experience

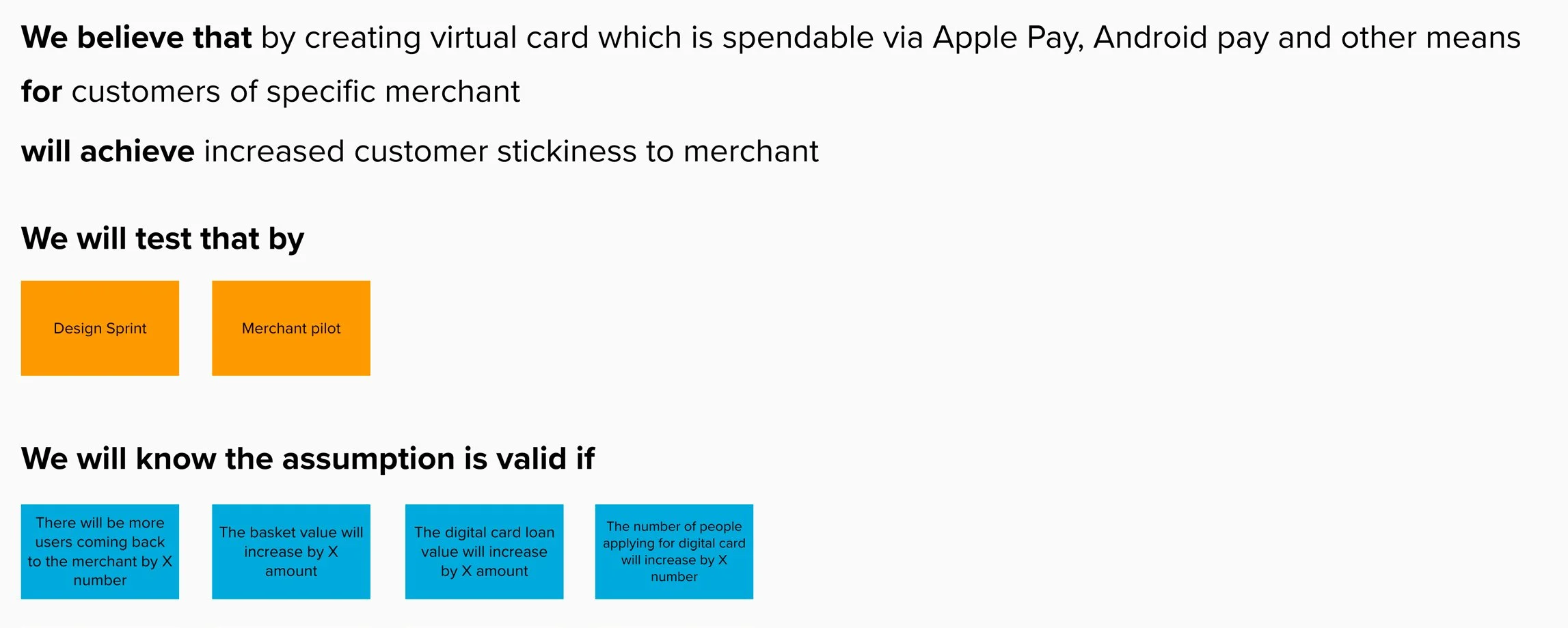

validate the product’s value through Value Proposition Canvas exercises, mapping user needs against product features

This phase helped translate the initial concept into a viable and scalable MVP.

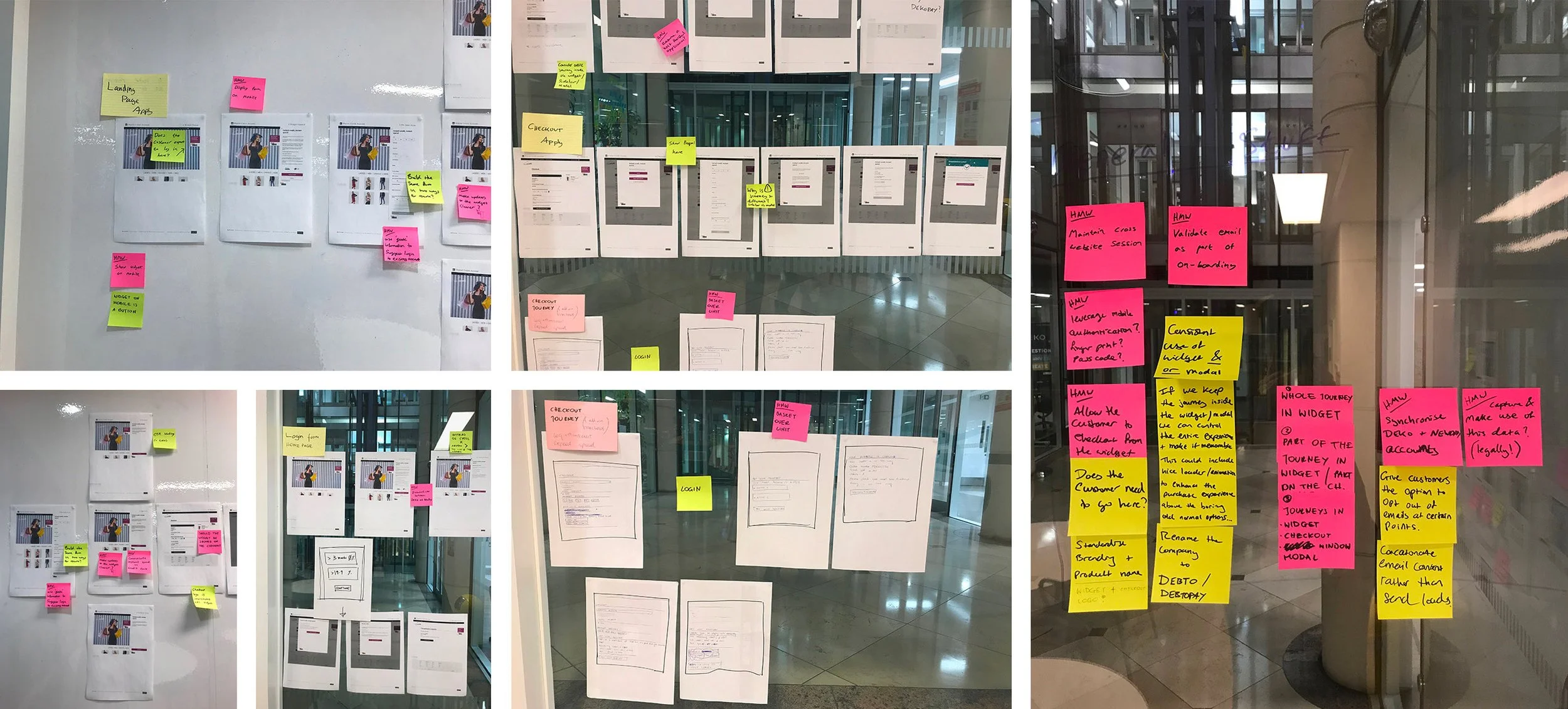

Design & Delivery

Building on the validated concept, I developed high-fidelity designs, refining the experience based on insights from the sprint and subsequent workshops.

The product combined several key elements:

a lightweight pre-qualification flow

upfront visibility of credit availability

a customer account area for managing credit and repayments

seamless integration into the merchant journey

The focus remained on creating a low-friction, high-confidence experience that supported both decision-making and ongoing account management. Because the product combined elements of finance application, affordability checking, virtual credit usage, and account servicing, the experience needed to feel significantly lighter and more approachable than traditional lending journeys. The experience was intentionally designed to position finance as a more integrated and supportive part of the shopping journey rather than a stressful end-stage checkout process. This required balancing commercial goals with customer trust, transparency, and usability.

The customer portal became an important extension of the overall product experience rather than a secondary feature. Beyond simply displaying account information, it was designed to provide users with greater visibility and control over their lending activity. The delivery phase also involved navigating the complexity of a multi-party ecosystem involving merchants, lenders, and Deko as the platform provider. Communication ownership, operational responsibilities, and user-facing interactions needed to remain seamless despite being distributed across different stakeholders and systems. The result was a significantly more connected finance proposition that moved beyond traditional retail finance flows into a more embedded and continuous customer relationship model.

Impact

The Digital Credit Account was very well received by both merchants and customers, particularly because it helped reduce uncertainty around affordability and purchasing confidence before checkout. By combining soft affordability checks, concise application flows, and ongoing account management into a single experience, the product introduced a more integrated and customer-centric approach to retail finance.

The proposition helped:

Increase customer confidence in financing decisions

Improve engagement and stickiness on merchant platforms

Support higher volume of finance applications driven by reduced uncertainty

Reduce friction traditionally associated with lending journeys

Successful adoption among small and medium-sized merchants

The product also demonstrated the growing importance of embedding finance earlier within shopping experiences rather than treating lending purely as a checkout utility. Users responded positively to having greater visibility and control over their available credit and ongoing account management. Over time, the platform continued evolving through multiple iterations based on customer, merchant, and lender feedback. Additional functionality, refinements, and operational improvements were introduced as the proposition matured and expanded.

Importantly, the product remained commercially successful beyond its initial launch phase and continued to operate as an active part of the wider platform offering. The proposition and its surrounding capabilities later became part of the broader NewDay ecosystem following acquisition, with the product continuing to evolve within the lending and embedded finance space.