Deko is a multi-lender payment platform designed to enable flexible checkout finance for both merchants and consumers. Its core proposition is to support any basket, anytime, anywhere, allowing businesses to offer tailored financing options seamlessly within the purchasing journey.

The platform connects multiple lenders in a single ecosystem, intelligently matching customers with suitable finance options to improve conversion rates and create a smoother checkout experience. By centralising lender integrations, Deko reduces complexity for merchants while increasing accessibility to finance for end users.

With a strong focus on scalability and continuous expansion, Deko evolves its offering to meet diverse business needs, positioning itself as a trusted partner in retail finance. Its product culture is grounded in clear values - doing the right thing, being bold, and operating as one team - which support collaborative delivery and customer-centric decision-making.

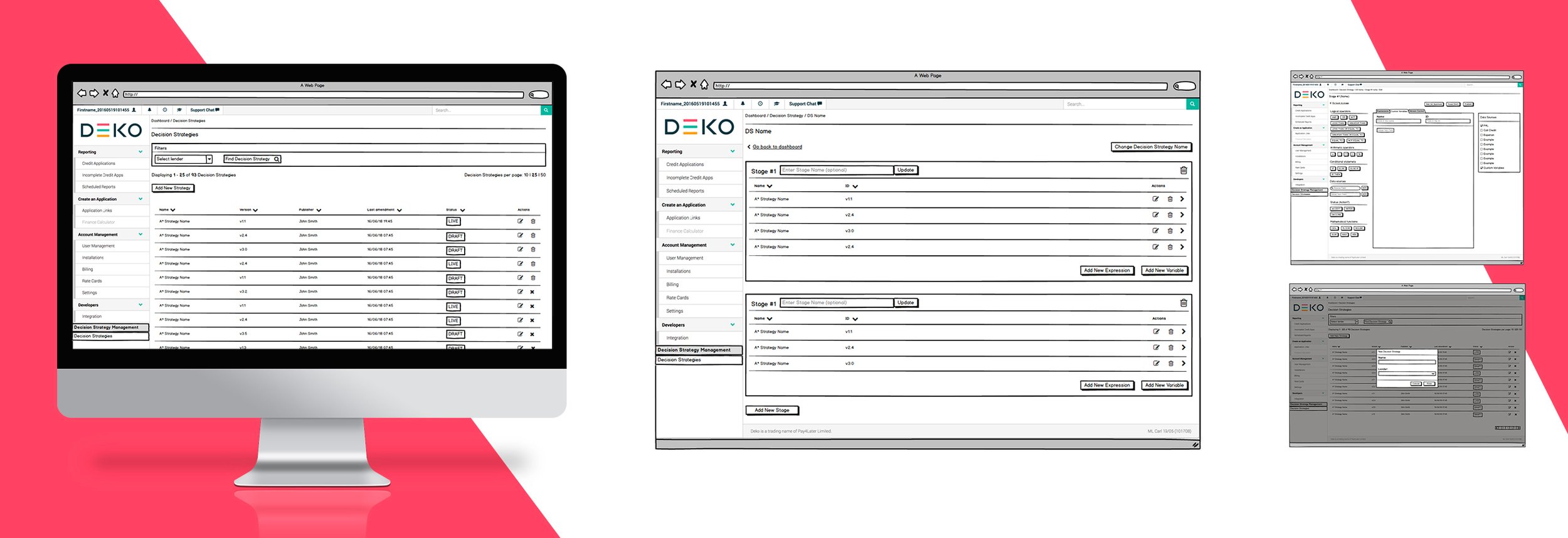

Lender Decisioning Engine

Enabling lenders to design, manage, and scale their own credit policies.

Overview

The Lender Decisioning Engine was designed as a self-serve back-office tool that allows lenders to create, manage, and evolve their own lending policies and decision rules. The aim was to shift from a developer-dependent model- where every policy change required engineering support - to a more scalable, product-led approach that empowers lenders with direct control over their decisioning logic. By bringing policy configuration into the product experience, the platform enabled lenders to respond faster to market changes, test new strategies, and tailor their risk models without operational friction. The project was a part of the idea to move the internal developers-dependencies onto the lenders, the same as in Lender Documents Management project.

My Role

Product Designer

I led the design of the decisioning experience end-to-end, including:

product discovery and lender research

workflow and interaction design

prototyping and usability testing

defining patterns within the Back Office Design System

close collaboration with engineering and product teams

The Challenge

The Decisioning Engine Tool was created to help lenders manage and configure their own lending policies, eligibility rules, and decisioning logic directly within the platform. Prior to this initiative, most rule changes relied heavily on internal engineering teams, creating operational bottlenecks, slower iteration cycles, and limited flexibility for lenders managing evolving credit strategies.

One of the biggest challenges was the high variability in lender processes and policy structures. Each lender approached decision-making differently, with unique internal governance, testing procedures, risk models, and approval workflows. The product therefore needed to support a wide range of use cases while remaining understandable and usable for non-technical operational users.

At the same time, we were redesigning and evolving an already existing internal tool originally built for developer use only. The existing experience contained inconsistent workflows, dead ends, unclear logic structures, and redundant interface elements, making it difficult to scale into a reliable external-facing product.

The challenge was not only to simplify an inherently complex system, but also to balance:

flexibility vs usability

powerful configuration capabilities vs operational clarity

technical complexity vs business accessibility

Because lending policies directly affected customer eligibility and business revenue, accuracy and reliability were critical. The product needed to support rapid policy iteration while maintaining confidence, traceability, and operational control for lenders.

Research & Discovery

The discovery phase focused heavily on understanding how lenders currently built, tested, and maintained lending policies within their organisations. Since decisioning processes varied significantly between lenders, it was essential to uncover common operational patterns while identifying opportunities for simplification and standardisation.

To gain deeper contextual understanding, we conducted a series of interviews and workshops with lenders, including visits to lender offices to observe existing workflows firsthand. This allowed us to better understand:

how policies were created and maintained

who was involved in the process

how changes were tested and approved

where operational pain points and inefficiencies existed

Alongside external discovery, a substantial part of the research involved auditing the existing internal decisioning tool used by developers. The system had evolved organically over time and contained inconsistent patterns, fragmented workflows, and limited usability considerations. Close collaboration with developers helped identify what functionality could be retained, what required simplification, and where entirely new interaction models were needed.

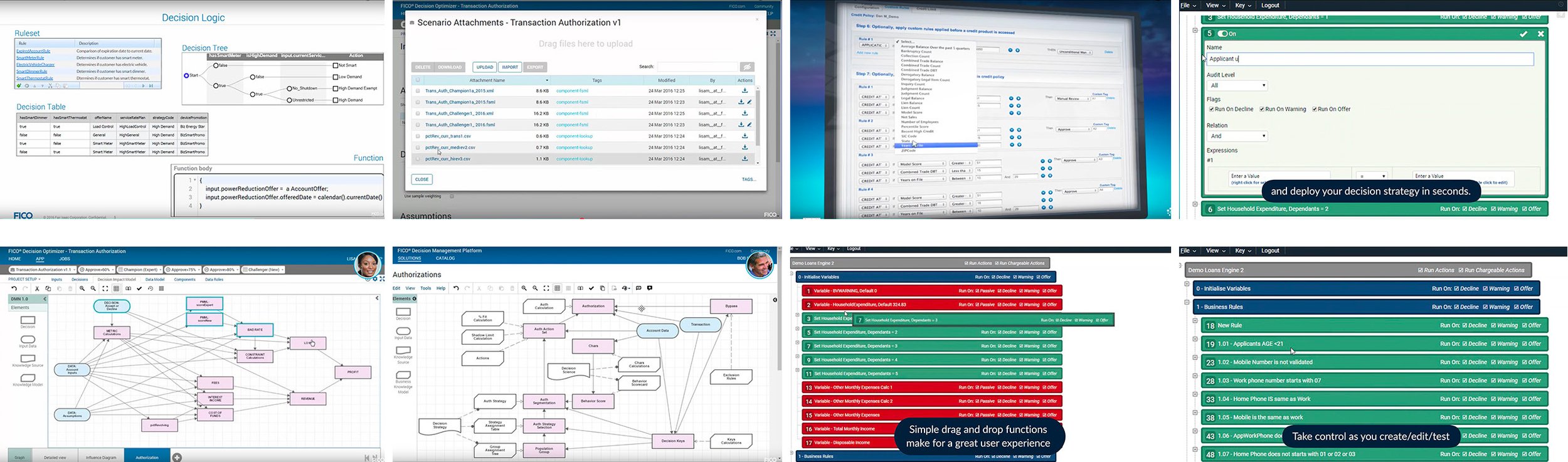

We also conducted broader market research into existing rule engines, workflow builders, and configuration platforms to understand established interaction paradigms for complex logic management tools. These explorations helped shape early product principles around modularity, visibility, rule hierarchy, and progressive disclosure of complexity.

The discovery process ultimately highlighted that the problem extended far beyond interface design. The real challenge was creating a scalable operational framework that could translate highly technical lending logic into a manageable and intuitive product experience for business users.

Design Approach

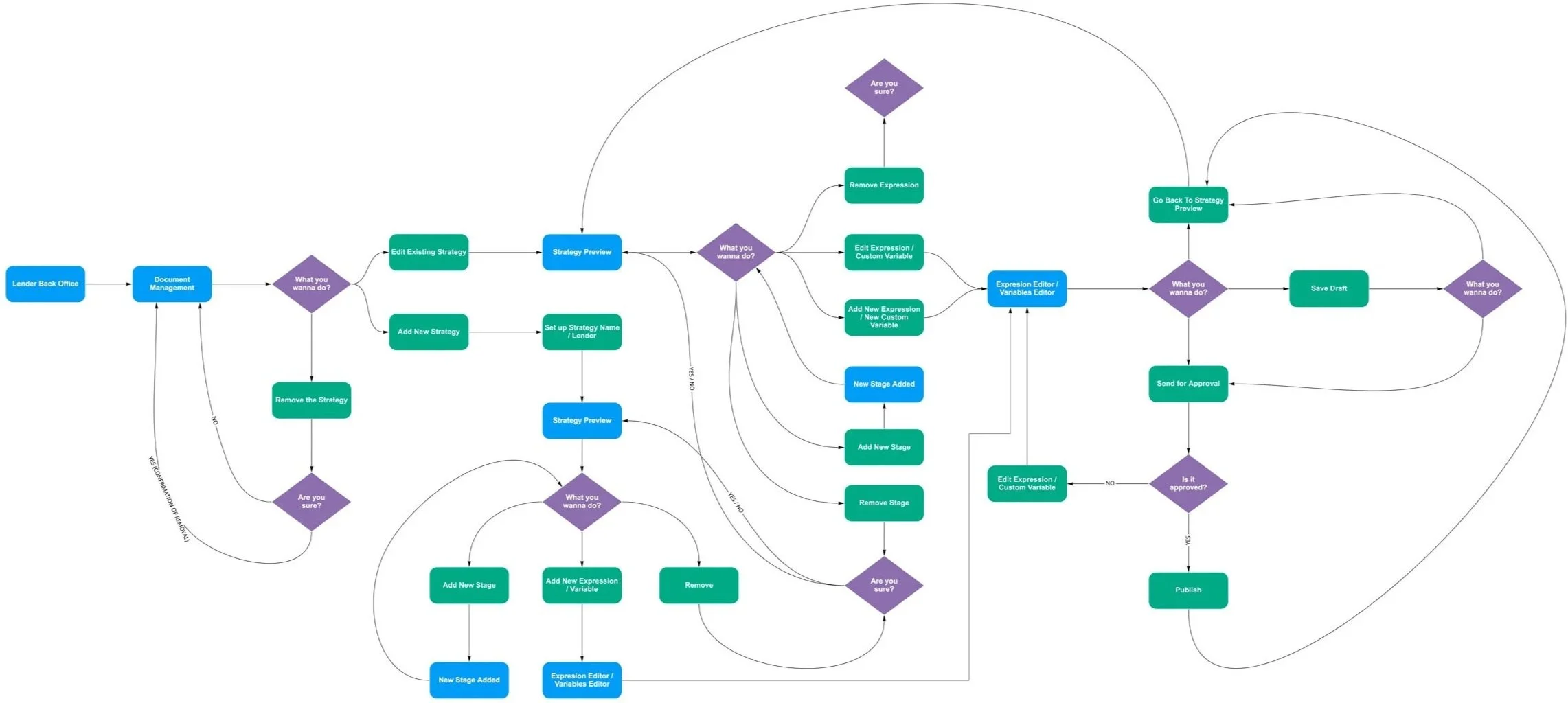

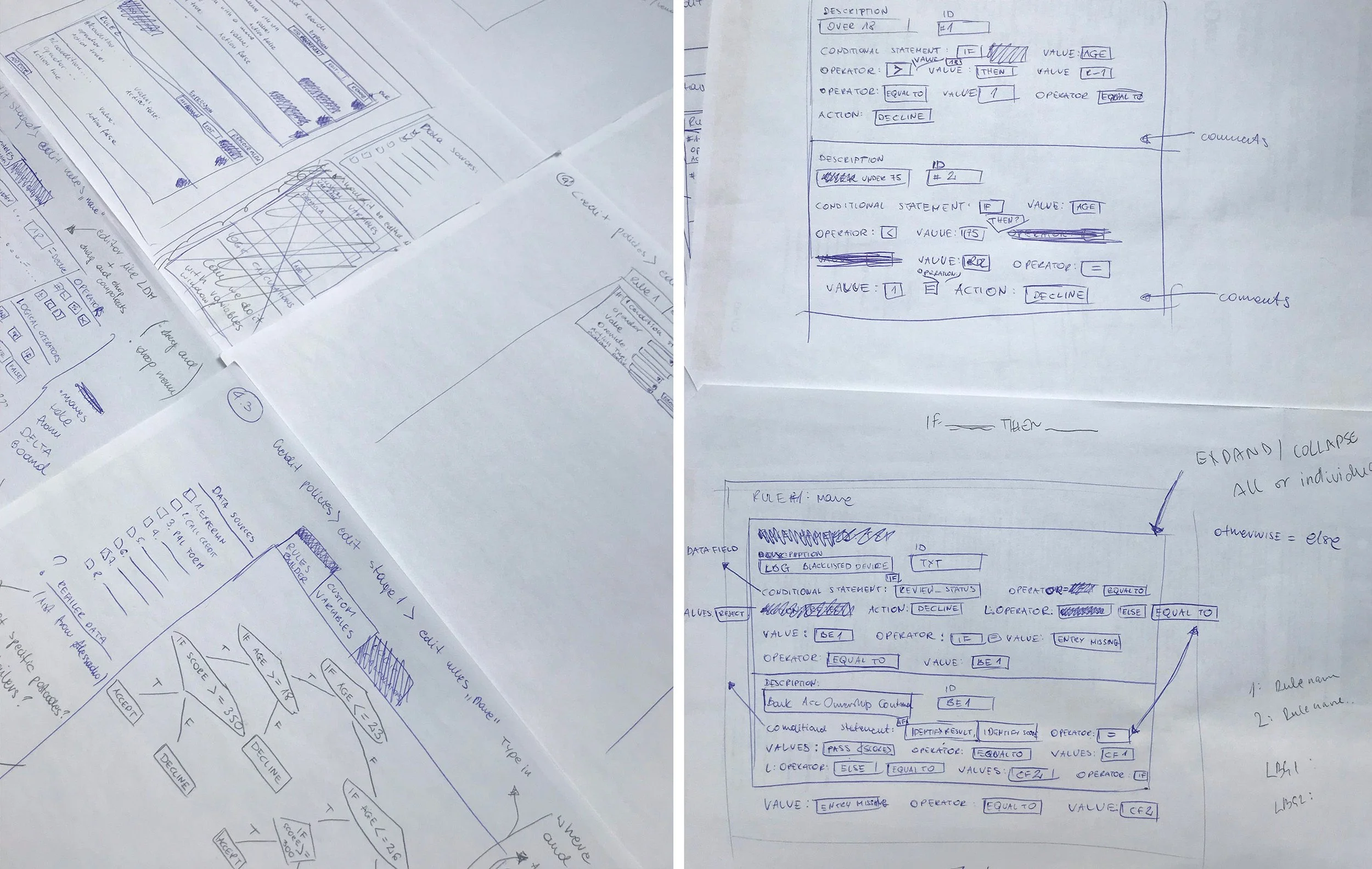

The design approach focused on progressively simplifying complexity without reducing the power and flexibility lenders required to manage their decisioning strategies. Because the product dealt with highly technical business logic, a major part of the work involved translating abstract rules, conditions, and dependencies into workflows that felt understandable and manageable for operational users.

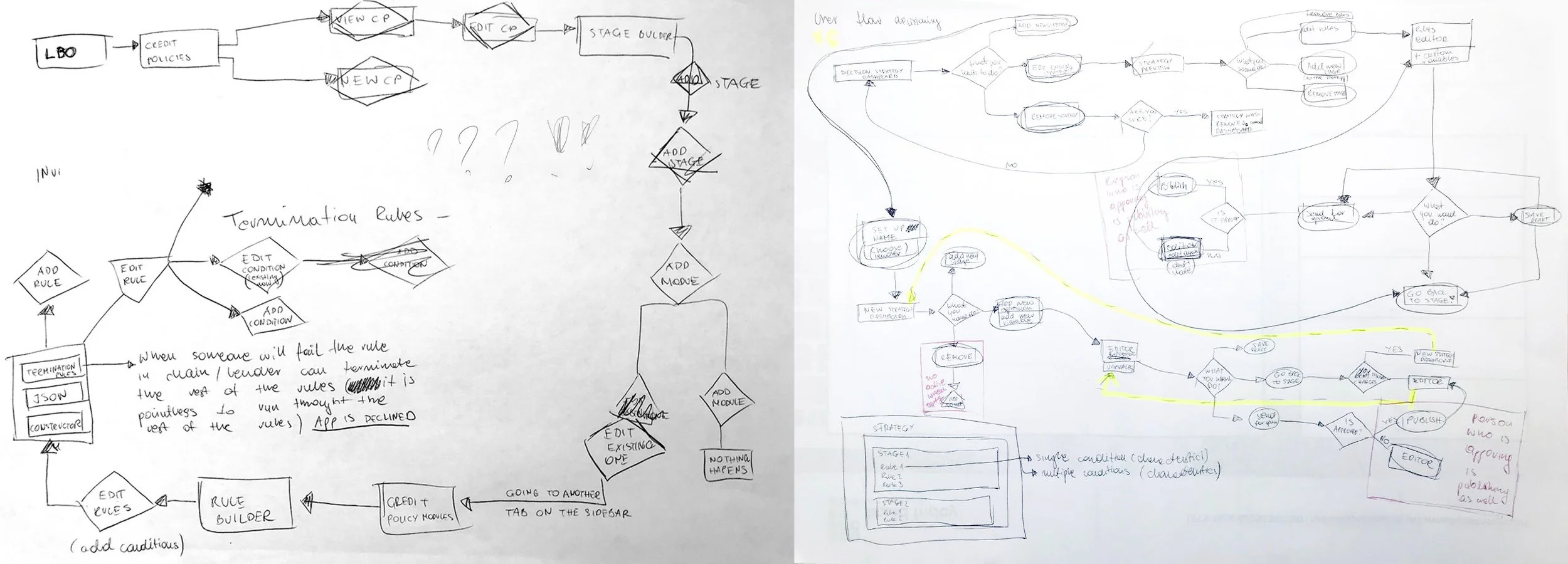

The early stages of design relied heavily on low-fidelity exploration, mapping logic structures, policy hierarchies, and rule relationships through sketches and wireframes. Interactive prototypes were then created to validate navigation flows, rule-building interactions, and visibility of decision states with lenders before moving into higher-fidelity design work.

Particular attention was given to:

reducing cognitive overload

improving visibility of rule relationships and dependencies

creating clearer editing and approval flows

ensuring users understood the impact of policy changes

maintaining confidence when interacting with highly sensitive lending logic

The design process was highly iterative and collaborative, involving continuous feedback loops with lenders, developers, product managers, and internal stakeholders. Due to the complexity of the workflows, prototypes became essential tools for validating assumptions early and reducing usability risk before development.

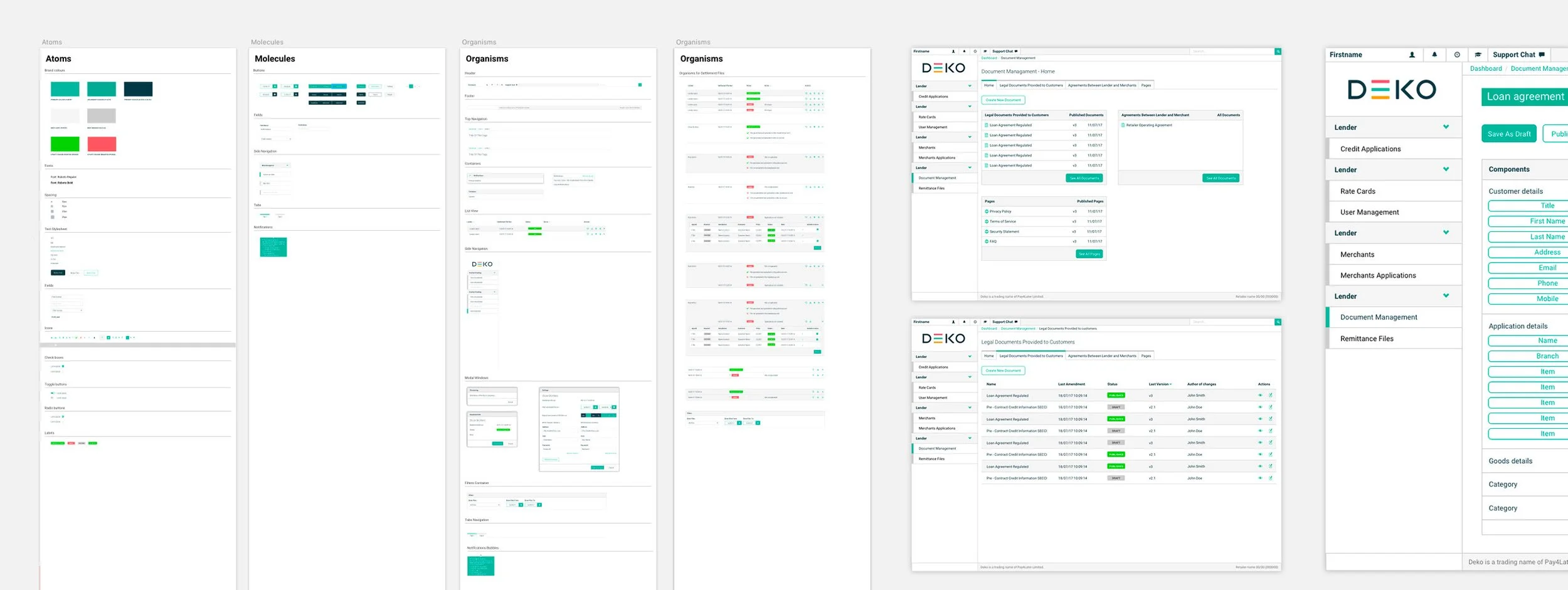

Design System & Visual Development

The Decisioning Engine Tool became part of the wider Lender Back Office ecosystem, meaning visual consistency and reusable interaction patterns were critical for scalability and long-term maintainability. The product therefore heavily leveraged the same Back Office Design Library that had previously been expanded during the development of the Lender Document Management Tool.

By this stage, the design system had evolved into a foundational layer supporting multiple operational products across the lender platform. Shared UI patterns, workflow components, tables, form structures, status indicators, and navigation behaviours allowed new tools to integrate more seamlessly into the wider ecosystem while reducing duplication across design and development.

The Decisioning Engine introduced additional complex patterns into the design system, particularly around:

rule configuration and nested logic structures

workflow management states

advanced forms and conditional interactions

visibility and status indicators

editing and approval flows

As the tool evolved, these new components further strengthened the maturity of the Back Office Design Library, helping standardise experiences across operational products while enabling faster iteration and more efficient collaboration with engineering teams.

The visual development phase focused not only on aesthetics, but on creating clarity within highly dense and technical workflows. Information hierarchy, spacing, grouping, and visual states played a major role in helping users navigate and understand complex decision structures more confidently.

Outcome & Impact

The decisioning engine marked a significant shift towards a more scalable and product-driven operating model.

Lenders were able to:

independently create and manage their policies

respond more quickly to changes in risk and market conditions

reduce reliance on engineering teams for operational updates

The product was well received and adopted by the majority of lenders, evolving through continuous feedback and iteration. Over time, additional functionality was introduced to support more advanced use cases, further strengthening its role as a core platform capability. The Decisioning Engine Tool significantly reduced operational dependency on engineering teams by enabling lenders to manage and evolve their own lending policies directly within the platform. This improved turnaround times for policy updates, increased flexibility for lenders, and created a more scalable operational model for the business.

The product was positively received across lenders due to its ability to simplify highly technical workflows while maintaining the flexibility required for complex credit strategies. Through continuous iterations and close collaboration with lenders, the tool evolved into a mature operational capability supporting a wide range of policy management scenarios.

Beyond usability improvements, the project also contributed to broader organisational maturity around operational tooling and product scalability. The introduction of reusable design patterns, modular workflows, and clearer rule management structures helped accelerate future product development across the lender ecosystem.

The Decisioning Engine continues to be used across multiple lenders, with ongoing enhancements and expanded functionality developed over time based on operational feedback and evolving business requirements.