Deko is a multi-lender payment platform designed to enable flexible checkout finance for both merchants and consumers. Its core proposition is to support any basket, anytime, anywhere, allowing businesses to offer tailored financing options seamlessly within the purchasing journey.

The platform connects multiple lenders in a single ecosystem, intelligently matching customers with suitable finance options to improve conversion rates and create a smoother checkout experience. By centralising lender integrations, Deko reduces complexity for merchants while increasing accessibility to finance for end users.

With a strong focus on scalability and continuous expansion, Deko evolves its offering to meet diverse business needs, positioning itself as a trusted partner in retail finance. Its product culture is grounded in clear values - doing the right thing, being bold, and operating as one team - which support collaborative delivery and customer-centric decision-making.

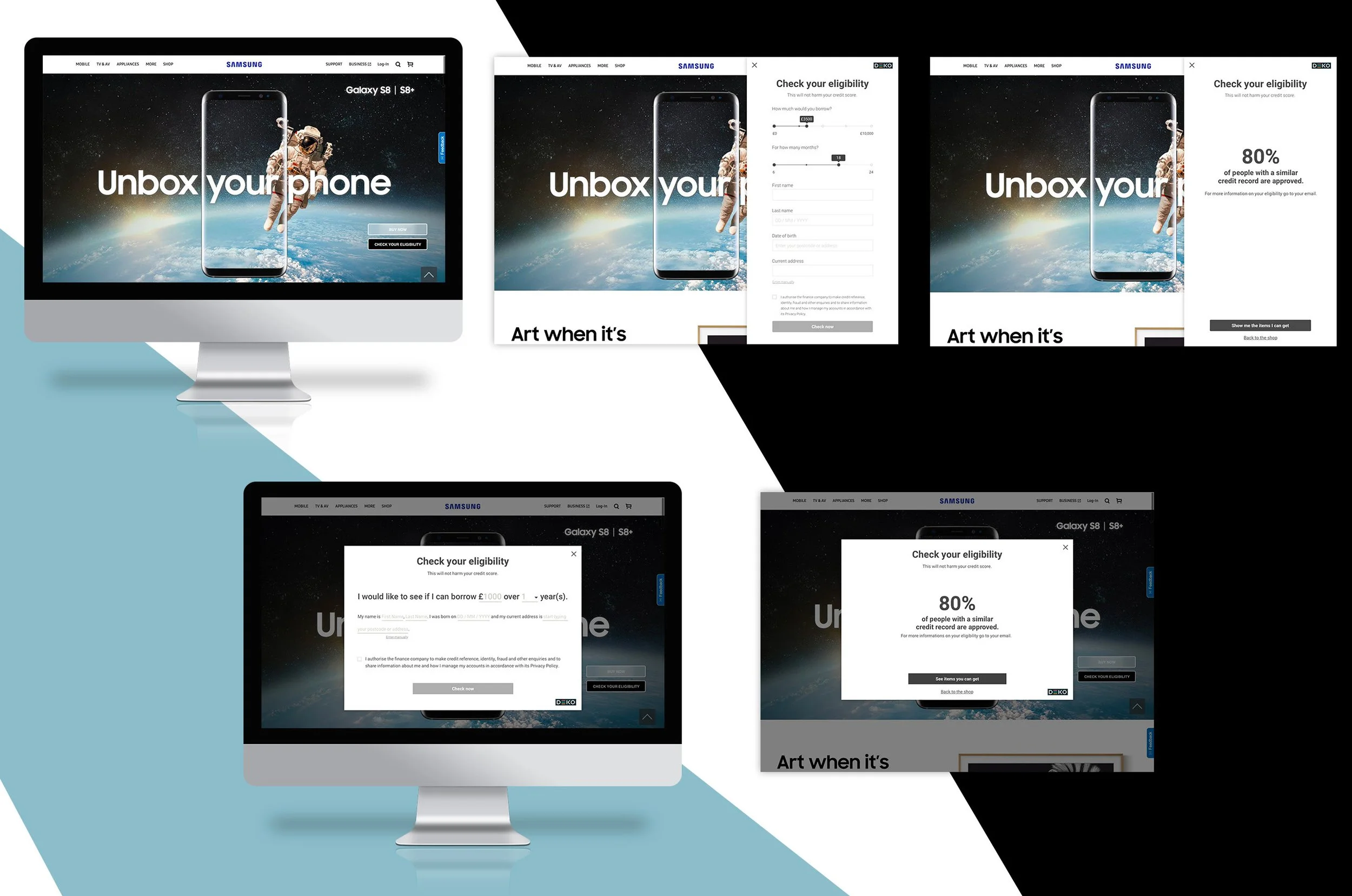

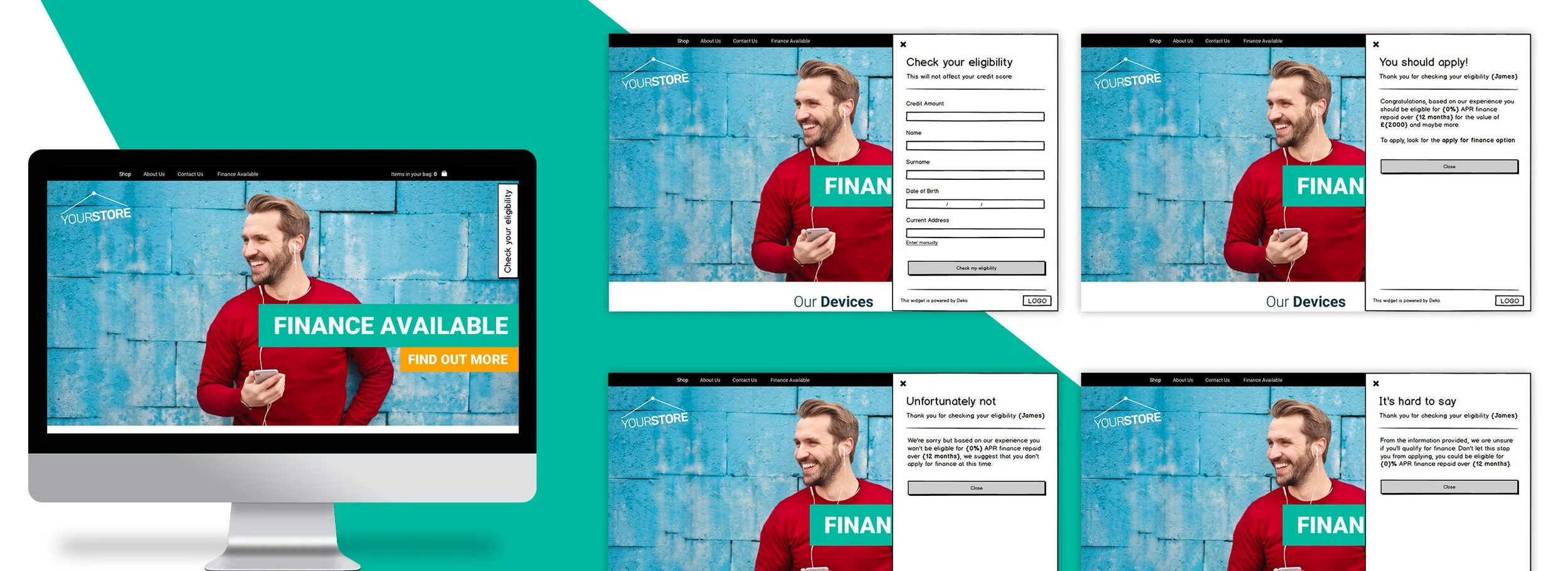

Pre-Qualification Tool

Reducing drop-off and increasing trust through upfront eligibility insights.

Overview

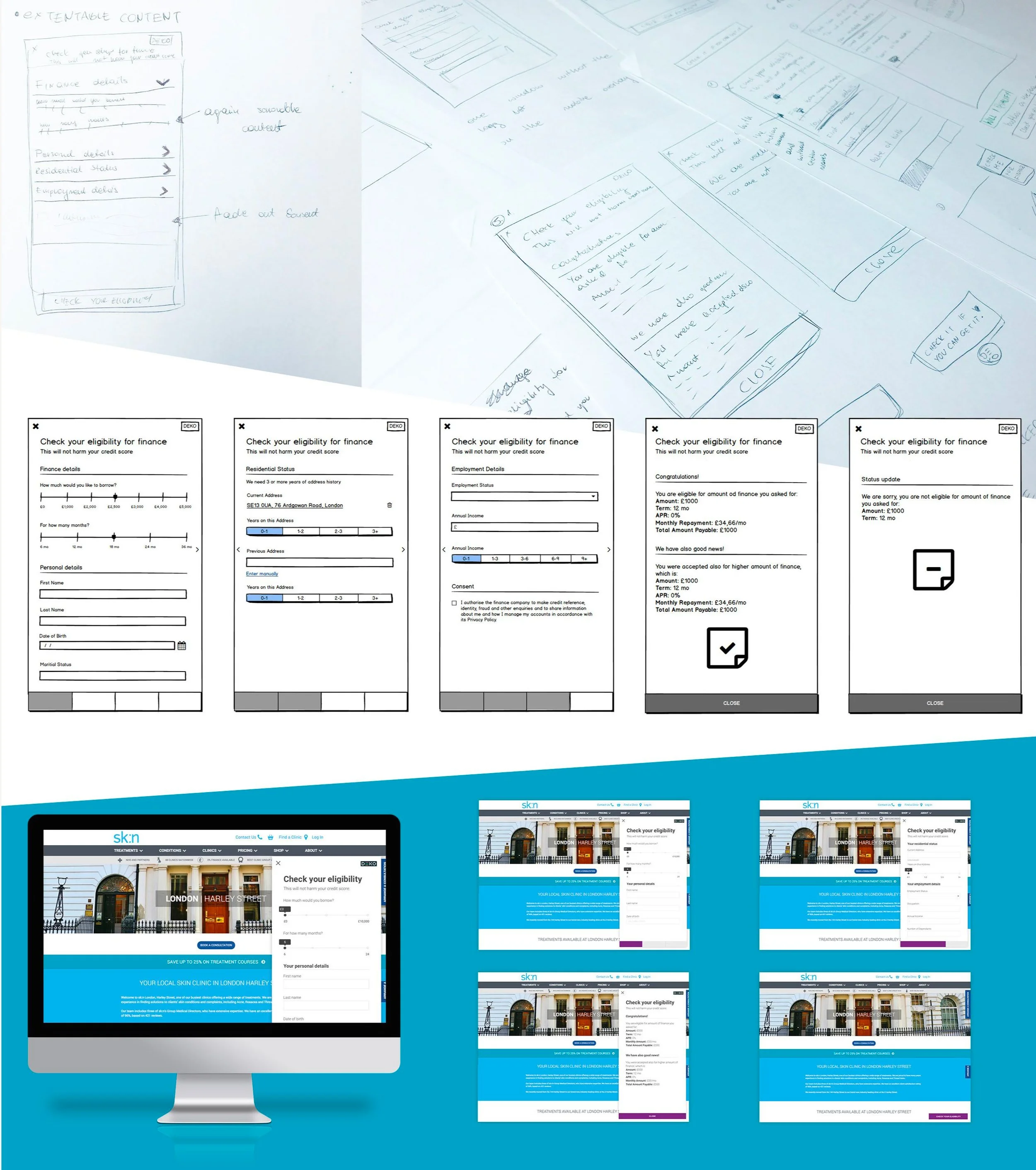

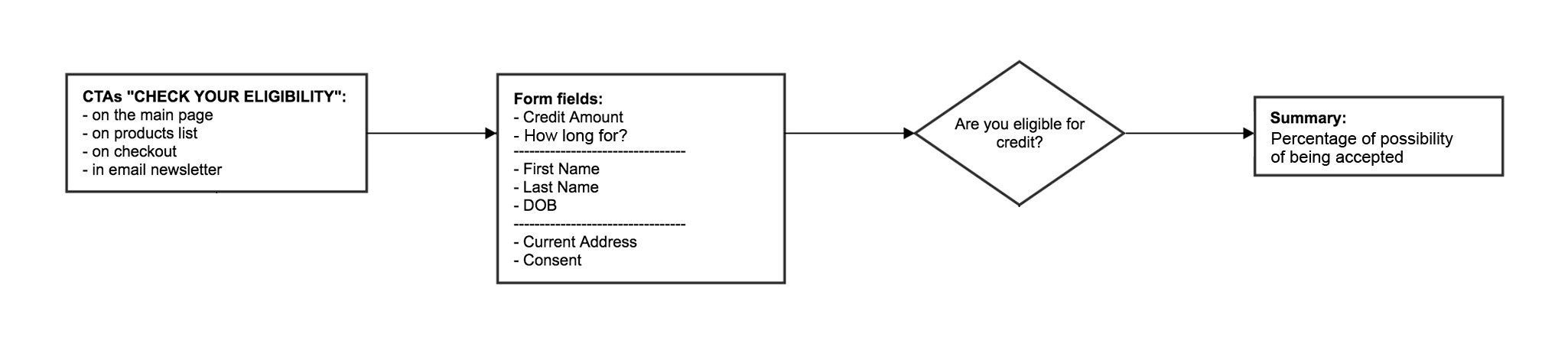

The Pre-Qualification Tool was introduced as a key enhancement to the Deko finance application journey, addressing one of the most critical drop-off points: user hesitation before applying for finance. Many customers abandoned the process due to uncertainty around approval and concerns about negatively impacting their credit score. The goal of this project was to introduce a low-friction, confidence-building step that would allow users to check their eligibility upfront through a soft credit check, without affecting their credit profile. By providing early feedback on loan eligibility and potential borrowing limits, the tool aimed to increase trust, reduce uncertainty, and improve conversion across the application funnel.

My Role

Product Designer

I worked within a cross-functional product team, contributing to:

product discovery and workshop facilitation

defining user journeys across multiple personas

designing wireframes, prototypes, and high-fidelity interfaces

running user testing and validation sessions

collaborating with product, engineering, and external stakeholders (lenders, merchants)

Team Structure

The project was delivered within a cross-functional team, including:

Product Designer (my role)

Product Manager

Frontend and Backend Engineers

QA (in later stages)

The Challenge

The project involved both product and business uncertainty.

From a product perspective, we needed to design an experience that could:

provide meaningful eligibility feedback with minimal user input

remain simple and fast, avoiding friction in the pre-application stage

balance clarity with the inherent uncertainty of credit decisioning

From a business perspective, there were several unknowns:

whether lenders would support the use of soft credit checks within their strategies

how to manage the cost of credit checks at scale

whether merchants would be willing to integrate the solution

how to design an MVP without a clearly defined precedent in the market

To address these uncertainties, we ran a series of discovery workshops to define the product direction and align stakeholders.

Product Goals

The Pre-Qualification Tool was designed to reduce one of the biggest behavioural barriers within retail finance journeys - customer hesitation before applying for credit. Research revealed that many users abandoned the application process due to concerns around being declined and negatively impacting their credit score through hard credit checks.

The product aimed to introduce a lower-friction entry point into finance applications by allowing users to complete a soft eligibility check, giving them more confidence and transparency before committing to a full application journey. At the same time, the proposition needed to create value across all three sides of the ecosystem - customers, merchants, and lenders.

Customers:

possibility of pre-qualifying for the specific amount of the loan without hitting their credit score using our short finance application form to reduce the drop-off rate and increase the trust in merchant service

boost customer confidence and minimise payment uncertainty ahead of shopping experience

Merchants:

pre-qualification tool is easy and quick to integrate with merchants

help them to boost customer confidence in their service and increase their revenue by reducing uncertainty ahead of shopping experience

Pre-qualification tool Increases average basket value what boosts revenue

Pre-qualification tool drives more traffic to an e-commerce site or physical store

Lenders:

pre-qualification tool is not lender specific and can be utilised by the range of the lenders

pre-qualification tool Increase revenue from lending activities what will boosts average loan values and applications increasing trust in their service

pre-qualification tool treats customers fairly by exploiting soft search technology

pre-qualification tool boosts merchant retention

The definition of these goals helped position the product not simply as a conversion optimisation feature, but as a broader strategic proposition connecting finance confidence, merchant growth, and lender scalability. Because standalone pre-qualification products for retail finance were still relatively uncommon in 2017, the initiative also represented an opportunity to shape a new category experience within the market.

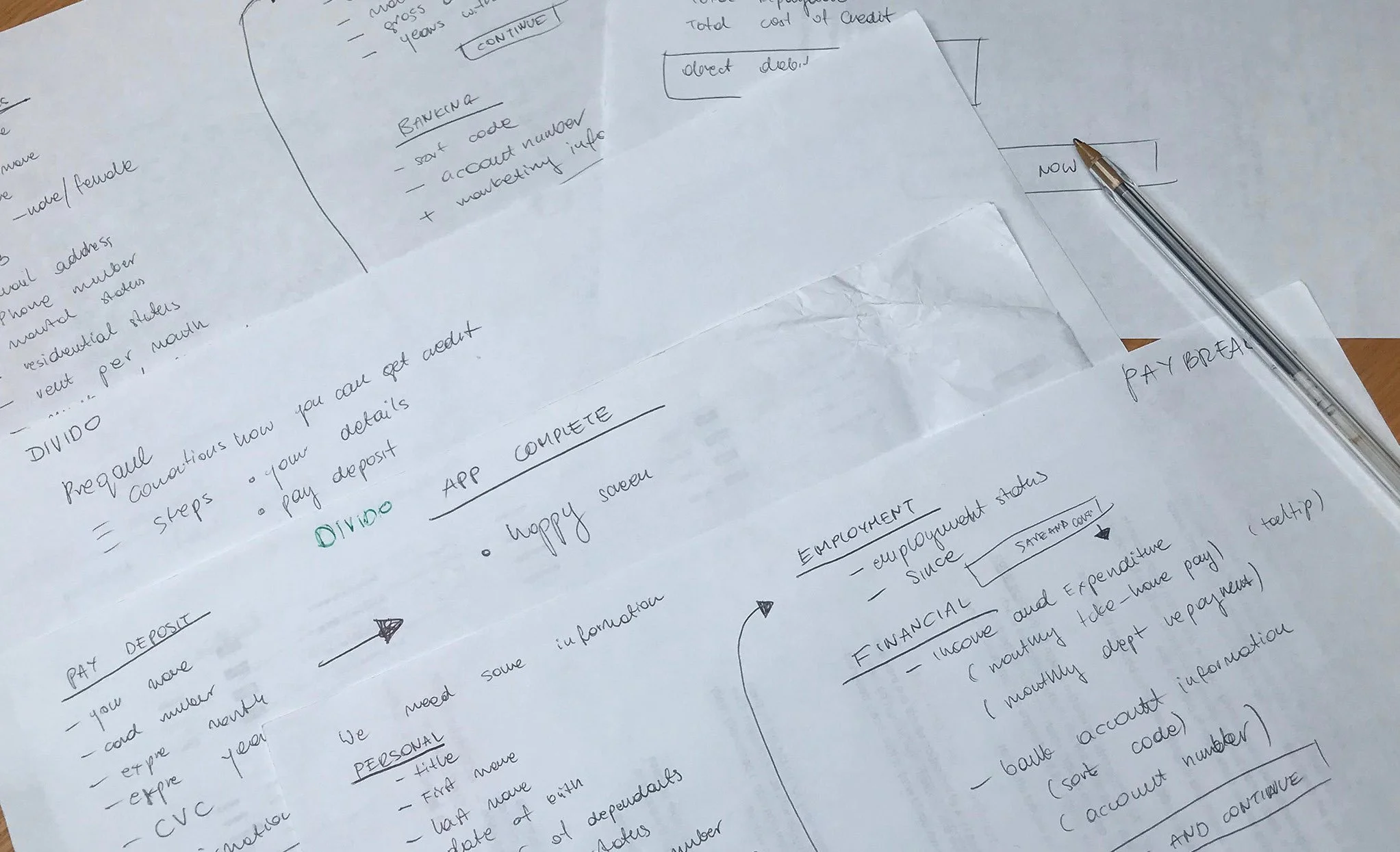

Research & Discovery

Upfront the creation we needed to do a lot of research on all the personas involved but also competitors. Before moving into design and validation, the discovery phase focused on understanding the behavioural, operational, and commercial dynamics surrounding finance hesitation and application abandonment. The research highlighted that uncertainty around eligibility and fear of damaging credit scores were major contributors to customer drop-offs before beginning full finance applications.

The product also introduced an entirely new operational model for merchants and lenders, meaning discovery needed to extend beyond end users into understanding:

lender appetite for soft search technology

merchant willingness to integrate the solution

operational feasibility of running eligibility checks

commercial sustainability of the proposition

Because there were very few comparable products in the retail finance space at the time, much of the early exploration relied on combining user research, stakeholder workshops, competitor analysis, and collaborative hypothesis generation to shape the initial direction of the MVP.

Competitors Research

Before we proceed with the first lo-fi prototype we made the competitors’ analysis and found out there are no standalone pre-qualification products for retail finance on the market. The existing solutions were created for credit cards only. That was a chance for us to create a product which doesn’t exist yet on the market but also came with a big challenge. The absence of established market patterns created both opportunity and uncertainty. Without strong industry benchmarks to follow, we had to define many of the product principles ourselves - from user expectations around soft checks through to communication patterns, lender integration flows, and merchant positioning. This required the team to move carefully between experimentation and commercial validation, ensuring the proposition remained understandable, trustworthy, and operationally viable for all sides involved.

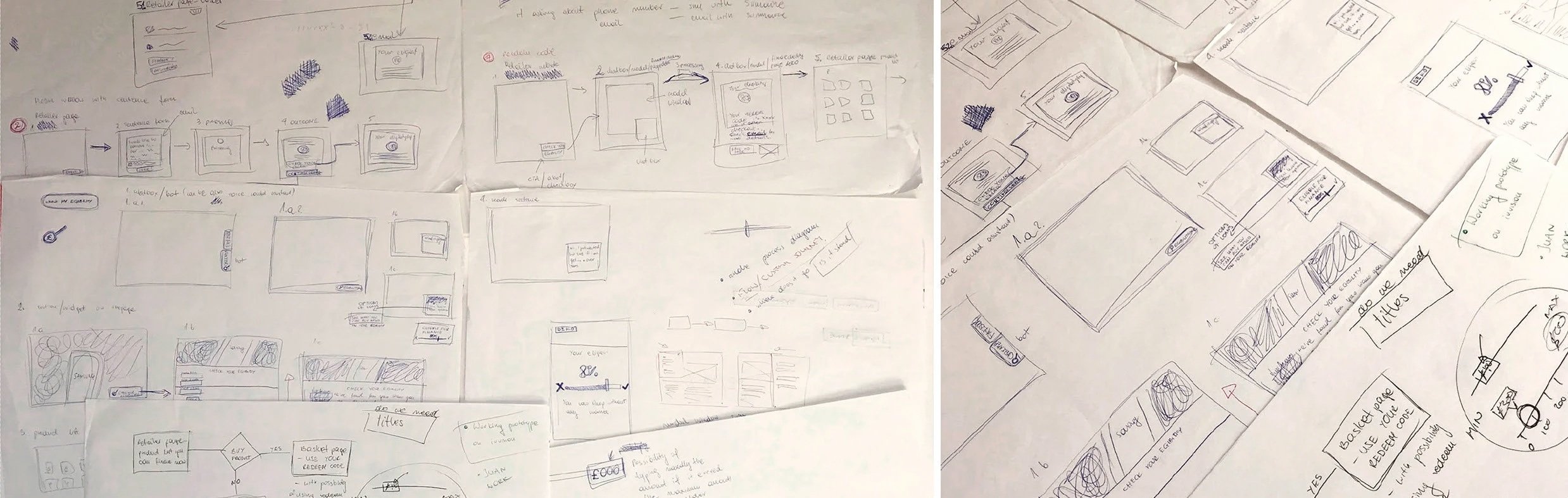

Design & Validation

We adopted a rapid, iterative approach, guided by a “fail fast, fail cheap” mindset. It became one of the core principles shaping the product design process. Given the uncertainty around user adoption, lender feasibility, and merchant integration, the team prioritised rapid experimentation and lightweight validation cycles before investing heavily into development.

Early concepts were translated into wireframes and clickable prototypes, which were tested in multiple rounds:

Initial in-house testing, focusing on clarity and usability

Iterative refinements, based on feedback around form length and output clarity

Guerrilla testing, conducted in real-world environments to gather broader insights

Particular attention was given to:

reducing perceived friction within the form

simplifying language around eligibility

communicating clearly that checks would not impact credit scores

ensuring users understood the outcome confidently

User interviews 1st round

We were inviting 3-5 users for the testing sessions in the initial phases of creating MVP for the first few weeks of the project. These early interviews helped validate the overall direction while exposing areas of hesitation, confusion, and trust concerns around finance applications.

User interviews 2nd round

Based on the first user interviews we prioritised some of the changes and did the iteration on the wireframes for further feedback. The second round of testing introduced guerrilla testing sessions in London cafes, allowing us to gather more spontaneous and diverse behavioural feedback. One of the key learnings was that users preferred clear, definitive outcomes (e.g. loan amounts) over abstract probability scores, and that minimising form length was critical to maintaining engagement.

The iterative testing cycles helped progressively refine:

the length and structure of the application flow

the framing of eligibility outcomes

the clarity of soft search messaging

the balance between reassurance and compliance requirements

Because the product proposition itself was relatively new for the market, validation became just as much about testing trust and understanding as it was about testing usability.

MVP Strategy

The MVP strategy focused on validating the commercial viability and behavioural impact of the proposition while minimising operational and financial risk during the early stages. Rather than building a fully automated decisioning ecosystem immediately, the first live version intentionally relied on partially manual lender checks behind the scenes. The MVP therefore prioritised learning speed and market validation over technical completeness. A key part of the strategy was also ensuring the product could remain lender-agnostic rather than tied to a single provider. This created stronger scalability potential and positioned the product as a broader platform capability rather than a lender-specific feature. By releasing a lean but functional version early, the team could quickly validate:

merchant demand

customer trust in soft search technology

conversion impact

operational feasibility

long-term commercial opportunity

The MVP ultimately proved that reducing uncertainty before checkout had significant value across the entire finance ecosystem.

Outcome & Impact

The product proved to be a strong commercial success for merchants, lenders, and customers and allowed the team to continue discovery activities for future iterations of the proposition. Key outcomes included:

increased customer confidence before finance applications

reduced hesitation around credit checks

improved merchant engagement and interest

stronger lender participation in soft search propositions

reduction of application uncertainty ahead of checkout

The introduction of soft eligibility checks helped fundamentally change how finance could be positioned within e-commerce journeys. Rather than finance being introduced only at the final checkout stage, the product enabled finance confidence to become part of the earlier shopping experience.

The tool also helped establish stronger relationships with merchants by supporting:

increased average basket values

improved customer trust

better conversion opportunities

lower payment uncertainty during shopping journeys

Internally, the project became an important example of how rapid experimentation, lightweight MVP delivery, and continuous validation could help shape entirely new product propositions within the finance industry.

Post-MVP Evolution

At the same time as the eligibility tool evolved, we started exploring a more advanced iteration focused on affordability checks. While the original pre-qualification flow helped users understand whether they were likely eligible for finance, the affordability proposition aimed to provide a more accurate picture of how much credit customers could responsibly access. Importantly, both solutions relied on soft credit search technology rather than hard credit checks, meaning users could explore finance options without negatively impacting their credit score. In the context of 2017, this was still a relatively progressive proposition within retail finance and represented a significant trust-building opportunity for both merchants and customers.

The affordability checks introduced additional complexity because the experience required:

more detailed financial information

heavier application flows

increased regulatory and compliance considerations

more advanced lender integrations

Balancing accuracy with simplicity became one of the key product challenges. The team needed to avoid recreating the same friction that existed within full finance applications while still providing meaningful affordability insights. The work on affordability checks later became the foundation for broader finance confidence and digital credit account propositions developed within the wider Deko ecosystem.